Hello There,

The last couple of months have been a little wild on the home front. My daughter Andie is "studying" abroad in Bilbao, Spain — translation: traveling, partying, and occasionally cracking a book. I'm all for it. I did the same thing at her age, and honestly I'm just jealous (and maybe I miss her a little).

My other daughter, Aubree, just won an emerging fashion award at the PBA BEACON Class of 2026 Announcement (watch her moment at the 15:45 mark). If you need a haircut, color, or anything else in that category, she's taking bookings — text me.

And I finally pulled the trigger on a small condo in Ft. Lauderdale. It's quirky, it's old, it's charming, and it's in a perfect spot to escape winter.

Now — down to business. There is a lotgoing on in the markets, and this month's main piece is one of my favorite topics. I hope you'll read it and come ask me hard questions later.

— Brad

Featured Event

Most advisors I talk to wantto offer venture capital to their clients. The challenge isn't demand — it's that the solutions available today weren't built with you or your clients in mind.

On April 30, I'll walk through what we built at Connetic: from our proprietary, data-driven sourcing engine that surfaces companies most VCs never see, to how those opportunities are now accessible through an electronically traded interval fund designed to scale across your practice.

I'll be joined by Kyle Hudson, founder of Stacklist(a Connetic portfolio company), who'll share the firsthand view of what it's like to build and grow with us as a capital partner.

If you've been waiting for a venture solution that actually works for your practice, this will be time well spent.

Featured Advisor Commentary

Shadow Valuations vs. NAV: What Most Advisors Are Reading Backwards

VCX launched at a $19 NAV. It traded as high as $575. Today it sits near $120 — and the underlying assets never changed.

In September 2025, SEC Chairman Atkins confirmed that registered products — closed-end ETFs, interval funds, BDCs, mutual funds — may hold private stocks. Registration means something: it is meant to make private markets accessible to everyone through the right structures. Since then, new products have hit the market at pace, and for advisors they can be genuinely hard to read.

Take VCX. Launched at a $19 NAV. Traded as high as $575. Today it sits closer to $120. The underlying assets never changed. Nothing fundamental shifted. But the price did — dramatically — and that gap tells you almost everything you need to know about a risk most advisors are completely misreading.

What Actually Happened

This wasn't performance. It was access.

VCX offered exposure to companies most investors can't reach — OpenAI, Anthropic, SpaceX. The float was tight, the story was compelling, and demand showed up fast. So the market did what it always does in that situation: it bid up access, not value. Early holders saw $575 — roughly a 2,900% premium to NAV — and did the rational thing. They sold. The price came back down. It still trades at a ~530% premium.

The Shadow Valuation

That spread between NAV and price isn't a traditional valuation signal. It's what I'd call a shadow valuation— or, more bluntly, a mirage. A premium investors willingly pay just to hold something they can't otherwise own. It's scarcity. It's narrative. It's demand. And it can grow very large, very fast.

The problem is that shadow valuations don't last. They exist only as long as access is limited. Closed-end funds trading at extreme premiums to NAV have a long history of mean reversion once that scarcity lifts — and it always does eventually. Academic research confirms this pattern: premium compression is the rule, not the exception, once competing access vehicles expand or the underlying assets become more liquid.

Grayscale Bitcoin Trust (GBTC) is the clearest recent parallel. Grayscale built scale by offering shares at NAV pricing in exchange for a 6-month lockup — the same structural playbook VCX is running. Once GBTC launched as the easiest access vehicle to bitcoin, it traded at market premiums of over 100% through the 2017–2022 mania cycle. Then other access opened up. At the time of this writing, GBTC trades around $55 against a posted NAV of $53.70. The premium disappeared. It always does.

The Expiration Date Nobody Mentions

Here's the real question: what happens when OpenAI trades publicly? When Anthropic or SpaceX lists?

At that point, anyone can buy them — directly, at market price, with no intermediary premium attached. In fact, at the market caps being discussed, most of us will end up with exposure essentially free through our S&P 500 funds. The entire rationale for paying a 500% premium to NAV through VCX evaporates. You weren't underwriting companies. You were underwriting scarcity. And scarcity, by its nature, goes away.

That's the risk advisors aren't pricing in. Not volatility. Not fundamentals. The fact that you're paying for something with an expiration date.

The Mirror Image: Why NAV Gets Misread

Now consider the opposite scenario. A non-traded fund launches at $10.00 and its NAV drifts to $9.85. No exchange listing, no premium, no discount — just NAV. The predictable reaction: "it's down."

But that reaction misunderstands what NAV is actually saying.

Private assets don't trade daily. NAV isn't a market price — it's a disciplined estimate built on comparable transactions, valuation models, audit standards, and documentation. That process has a well-documented character: it tends to be lagged, smoothed, and conservative. Private equity and venture funds are required to mark assets to fair value, but that value is typically anchored to models and judgment rather than live transactions. The FASB standards governing this (ASC 820) explicitly acknowledge the absence of observable market prices in Level 3 assets.

In practice, that conservatism means assets are frequently carried below what they ultimately sell for. Research consistently finds that private investments are realized at premiums to their last reported NAV — particularly in exits and secondary transactions. That $9.85 NAV may not be a warning sign. It may be an honest, conservative mark on assets that haven't had a liquidity event yet.

The Behavioral Trap

The irony is that advisors often read these signals backwards.

What Most Advisors See

VCX at $575 → "This is working."

VCX at $120 → "Something broke."

NAV at $9.85 → "This is underperforming."

What's Actually True

VCX at $575 = inflated shadow valuation

VCX at $120 = premium compression, still expensive

NAV at $9.85 = honest, possibly conservative — maybe a discount

When you buy at NAV, you're not paying for narrative or access or the demand of whoever bought before you. You're paying a price already filtered through valuation policy, audit scrutiny, and institutional discipline. In many ways, it's cleaner than a public market price — because public prices bake in sentiment. NAV doesn't.

The Real Question

Every advisor evaluating these structures is making a version of the same choice: pay a premium for access that may disappear, or buy assets at a price that may already be conservative?

VCX didn't create value. It created a shadow valuation — one with an expiration date. NAV-based investing doesn't look exciting. It's not supposed to. It's just telling you the truth.

If you're paying a premium for access today, you need to understand exactly what happens the day that access becomes free.

Sources

Financial Accounting Standards Board. ASC 820: Fair Value Measurement. FASB, 2011 (updated 2018). Link

CFA Institute. Global Investment Performance Standards (GIPS) for Private Markets. 2020 Edition. Link

Harris, Robert S., Tim Jenkinson, and Steven N. Kaplan. "Private Equity Performance: What Do We Know?" Journal of Finance, Vol. 69, No. 5 (2014), pp. 1851–1882. Link

Phalippou, Ludovic, and Oliver Gottschalg. "The Performance of Private Equity Funds." Review of Financial Studies, Vol. 22, No. 4 (2009), pp. 1747–1776. Link

Lee, Charles M.C., Andrei Shleifer, and Richard H. Thaler. "Investor Sentiment and the Closed-End Fund Puzzle." Journal of Finance, Vol. 46, No. 1 (1991), pp. 75–109. Link

Cherkes, Martin, Jacob Sagi, and Richard Stanton. "A Liquidity-Based Theory of Closed-End Funds." Review of Financial Studies, Vol. 22, No. 1 (2009), pp. 257–297. Link

Preqin. Global Private Equity & Venture Capital Report, 2023. Link

Private Company Highlight

Coolest Private Company of the Month: Narratize

A Northern Kentucky, female-founded AI company you should know.

Yes — read that again. NKY. AI. Female-founded.

Narratize — founded by Katie Taylor and Catherine O'Shea — is helping large enterprises like Delta and Goodyearturn deep technical knowledge into clear, compelling narratives at scale. It's the kind of quietly category-defining work that tends to come out of operators who've lived the problem.

If you run a company (or know someone who does) wrestling with how to tell a complicated story well, this is a name worth knowing.

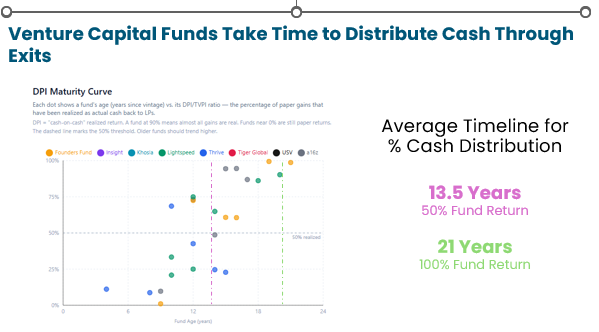

Data Corner • Chart of the Month

Good Things Come to Those Who Wait

Some of the best-performing funds in the world share one unglamorous trait: time. Venture capital rewards patience — and the data makes the case more clearly than any narrative can.

Connetic Corner

Behind the Curtain: KPIs, Scorecards, and a 9-Person AI Advisory Board

We've shifted into high-gear performance mode at Connetic — KPIs, scorecards, and milestones are dominating board conversations. But the most interesting shift internally has been how we're using AI.

We started on ChatGPT, moved to Claude, and haven't looked back. The output quality our development and valuation teams are getting is genuinely impressive. For fun, I had Claude build me a nine-person advisory boarddrawn from the complete written works of Milton Friedman, Elon Musk, Seth Godin, Scott Galloway, "Future Brad Zapp," Thomas Sowell, Aristotle, Marcus Aurelius, and Jesus Christ. I ask them the hardest questions in my life and they write a consensus answer — with dissenting opinions when they disagree. (Jesus dissents a lot. It's hilarious.)

If you aren't messing with AI yet, you need to be. It's effective and fun.

Dates to watch: Quarterly report drops in the next couple of weeks. If you're an advisor and you missed our last IVs & Bourbon Rocket Pitchesevent, I'm running another in May — not to be missed.

FOLLOW CONNETIC VENTURES

in

Some statements herein may express future expectations and forward-looking views based on Connetic's current assumptions. Statements about companies, securities, or other financial information represent personal beliefs and viewpoints of Connetic or the respective third party. These statements may involve known and unknown risks and uncertainties, potentially leading to different results than those implied or expressed. All content is subject to change without notice.

The information herein was obtained from various sources. Connetic Ventures does not guarantee the accuracy or completeness of information provided by third parties. The information in this newsletter is given as of the date indicated and believed to be reliable. Connetic Ventures assumes no obligation to update this information, or to advise on further developments relating to it. Connetic Ventures offers investment advisory services and is registered with the U.S. Securities and Exchange Commission ("SEC"). SEC registration does not constitute an endorsement of the advisory firm by the SEC nor does it indicate that the advisory firm has attained a particular level of skill or ability. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Form ADV Part 2A & 2B can be obtained by visiting: https://adviserinfo.sec.gov and search for our firm name.

Connetic RIA, LLC | 910 Madison Ave. | Covington, KY 41011